Protecting Yourself from Check Fraud

Example of Check Fraud and Poor Customer Service at Charles Schwab

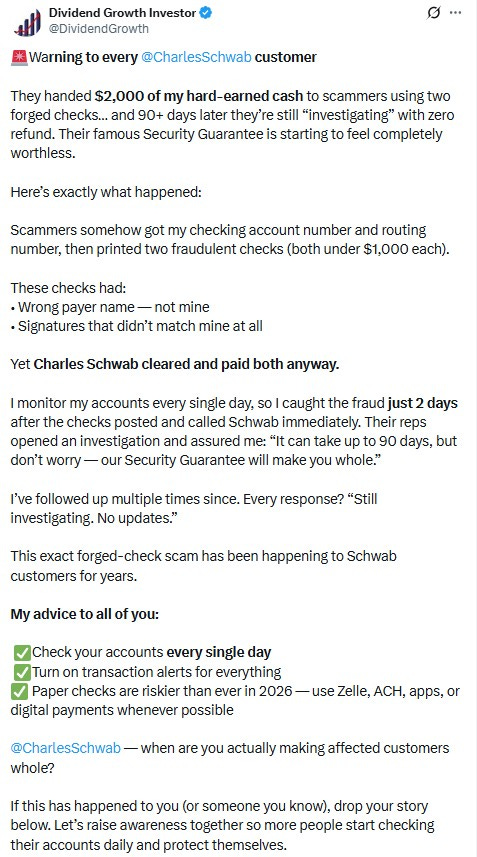

One of my early BankDealsBlog readers who has become a dividend stock investing expert just published a Twitter/X post describing how scammers stole about $2,000 via check fraud from his Charles Schwab account. He did all the right things, but he has yet to be reimbursed after more than 90 days. Here’s the link to his X post. I’ve included a snapshot of the post for those who don’t have access to X:

I see three issues of concern for the dedicated savers of DQ:

First, beware of Charles Schwab and Charles Schwab Bank. I think most people think Charles Schwab is just a brokerage firm. However, its primary banking subsidiary, Charles Schwab Bank, SSB, is one of the largest banks in the nation with total assets of $254 billion as of December 31, 2025. As a comparison, Ally Bank has only $185 billion in total assets.

I remember writing about Charles Schwab Bank around 20 years ago when they offered competitive rates on the Schwab Bank Investor Checking account and the Schwab Bank Investor Savings account. Competitive rates at Charles Schwab didn’t last, but at least the Bank maintained nice banking features and provided good customer service. Based on this check fraud case, I have serious doubts about the quality of their customer service.

The second issue about this check fraud case is to remember to regularly monitor your bank accounts. Transaction alerts can also help you monitor bank account activity. If fraud occurs, it’s important to catch it early and report it to the bank. If you wait too long, the bank may be able to avoid liability for your loss. Regulation E deals with fraud related to electronic transfers and the Uniform Commercial Code (UCC) covers paper check fraud. Under Regulation E, a consumer’s responsibility for unauthorized electronic transactions is capped at $50 if you report the issue within two business days. If you report it within 60 days, your maximum liability increases to $500. This OCC page is a useful resource in preventing and dealing with check fraud.

Lastly, be careful with checks and your account numbers. Paper check fraud continues to be a major issue. Try to avoid mailing paper checks and paying with paper checks. Use online bill pay and credit cards instead.

This might also be a reason to avoid having too many checking accounts or money market accounts that allow you to write paper checks. A few online banks that offer checking accounts don’t allow paper checks to be written. CIT Bank’s eChecking is one example. This is how CIT Bank describes its eChecking account in its FAQs:

This is a checkless checking account. Traditional checks will not be paid on this account. Although you may be able to create and purchase checks from a third-party vendor, all checks written payable against your eChecking will be rejected by the system and mailed back to the payee with a notice.

One benefit of keeping your money at banks is that your money should be protected. The FDIC protects against losing your money from a failed bank, but it doesn’t specifically protect you from loss due to fraud. Regulation E and UCC are designed to help consumers, but as this case shows, it may be impossible to be 100% safe from loss..

How do you protect yourself from check fraud? Have you experienced similar issues at Charles Schwab or at other banks? How long did it take for your bank to refund you the lost money? Comments are very much appreciated!

Ken, someone I assist regarding financial matters put a 5-figure check payable to his attorney in a USPS mailbox, even though I've given the warning not to do it that way. A thief who was able to obtain a master key to the mailbox hit the jackpot, and was able to check wash it and steal the money because it took over week before the lawyer advised they have not received payment.

We need more like you who are doing this fabulous service trying to protect people.

Hi Ken, great to see you here and thank you for this and your always excellent posts.

Dividend Growth Investor’s tale is all to familiar these days. I have yet to experience being a victim of check fraud myself but know someone who has and the final outcome was not good.

I try to avoid paper checks and do all transactions digitally except in very rare circumstances where it is unavoidable. I have a cave dwelling family member who insists on payment by check every time I need to reimburse them for anything and I am trying to gently entice them into the 21st century. They still pay virtually everything by paper check. I will share your post with them to see if it can set off a lightbulb (maybe I should say an LED bulb to stay on point).

The only thing I can think of adding to your protection plan is this:

I have a checking account I keep a minimum balance in until I need to write a paper check. I opted out of overdraft protection on this account so that overdrafts will not be covered. I fund the account with the amount of the check just before writing it. This way I think it mitigates my exposure in the event someone tries to deposit a large fraudulent check. Hopefully it will be rejected. PS: Try to pick a bank that is not very courteous so they won’t cover a fraudulent check as a “courtesy.”

I think the recommendations given in your post are all good ones which I practice myself and have never had an issue with check fraud in over 50 years of banking and investing. Of course no one with an account that takes paper checks, including me, is ever 100% immune. I think the financial industry would do well to encourage offering a no paper check option as standard on all checking accounts and it would result in a significant reduction of this kind of fraud.